Radiation Sources Poster – HAZCOM

Be aware of orphaned radioactive sources as they pose an extreme danger to plant and person and would be very difficult to […]

+27 12 380 0900 saisi@saisi.org

South Africa’s dependence on imported steel is no longer a short-term or cyclical issue — it has become a structural challenge with serious implications for the domestic industry, downstream manufacturing, and national economic resilience.

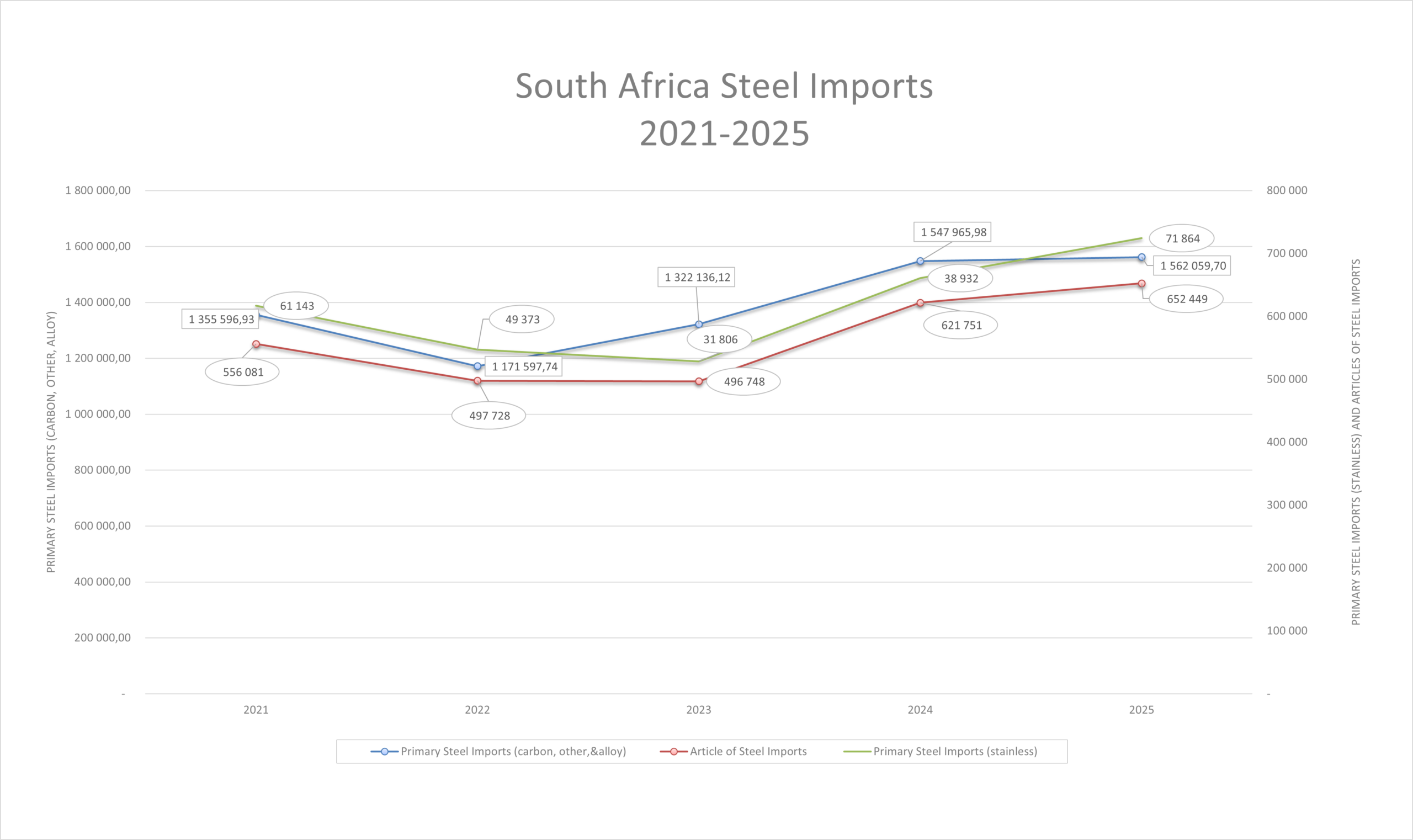

SAISI’s analysis of primary steel imports (2021–2025) shows carbon steel imports reaching 1.56 million tonnes in 2025, following only a brief pause in 2022. This confirms sustained and elevated import pressure on the domestic industry.

The pattern extends beyond carbon steel. Stainless steel imports surged by 78% year-on-year in 2025, alongside increased price volatility and shifting import strategies. More concerning is the growing focus on value-added products, accelerating de-industrialisation rather than enabling downstream growth. Articles of steel (HS 73) rose from 556,081 tonnes in 2021 to 652,499 tonnes in 2025, biggest drivers include structural steel, small diameter pipes, rail & railway material, wire rope & cable, kitchen and household articles.

Data shows the opposite: import volumes increasing while prices remain suppressed, a clear signal of injurious pricing behaviour aimed at market capture.

This pressure is highly targeted. Hot-Rolled and Hot-Dipped Galvanised steel account for over 60% of carbon steel imports, directly undermining the backbone of South Africa’s manufacturing and construction sectors and placing multiple local producers at risk.

Downstream and Economic Consequences

The Stakes Are High

This is not just a commercial issue, it is a national economic and strategic concern. If unaddressed, continued import pressure will:

The consequence of inaction is clear: plant closures, permanent loss of industrial capability, and weakened economic sovereignty. Concentrated imports from the Far East, combined with persistent price suppression, are displacing local production, threatening jobs, investment, and long-term resilience.

© SAISI 2026. All rights reserved.