Global Steel Production Trends: Analysing January 2024 Figures and South Africa’s Strong Start in the New Year.

In January 2024, the global crude steel production landscape witnessed various shifts and trends, as reported by the World Steel Association (worldsteel). Despite a slight dip in worldwide production compared to the previous year, several regions showcased notable developments, with Africa notably standing out with a significant increase.

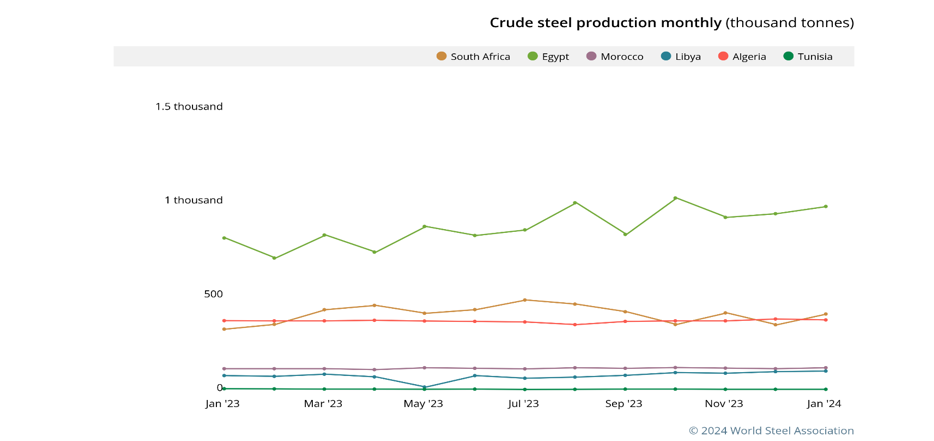

According to worldsteel’s data, the total crude steel production for the 71 countries reporting amounted to 148.1 million tonnes (Mt) in January 2024, reflecting a marginal decrease of 1.6% compared to January 2023 figures. However, Africa’s production, standing at 2.0 Mt during the same period, experienced a remarkable upswing of 16.3% from the previous year.

Asia and Oceania combined contributed 107.6 Mt to the global production, indicating a decrease of 3.6%. The European Union (EU 27) produced 10.2 Mt, a slight decline of 1.8%, while Europe, excluding the EU, witnessed a substantial increase of 22.5% with a production of 3.9 Mt. The Middle East recorded a noteworthy growth of 23.1%, reaching a production of 4.7 Mt.

North America’s production stood at 9.2 Mt, experiencing a decline of 2.1%, while Russia, other CIS countries, and Ukraine collectively produced 7.2 Mt, showcasing a 4.0% increase. South America, however, faced a downturn with a production of 3.4 Mt, indicating a decrease of 6.3%.

Of particular interest is South Africa’s performance in the steel production arena. In January 2024, South Africa’s crude steel production surged to 406,600 tons, marking a significant uptick of 24.8% compared to the same period in 2023 when it stood at 325,800 tons.

Trade Dynamics: A Look into South Africa’s Steel Sector

In the realm of global trade, South Africa’s steel industry has been a pivotal player, exhibiting both challenges and triumphs in recent years.

Trade Balance Shifts:

In 2021, South Africa grappled with an overall trade deficit, largely attributed to significant shortfalls in flat products. However, by 2022, the nation witnessed a notable improvement in the trade balance, propelled by positive performances in intermediate products, sections and bars, and wire. Despite continued positive contributions from these sectors in 2023, widening trade deficits in flat products led to an increased overall deficit of R1.9 billion.

Primary Steel Imports and Exports:

2023 saw a significant rise in the import of primary carbon, alloy, and other steel products in South Africa, excluding semis, stainless steel, and drawn wire. The total volume reached 1,330,546 tonnes, marking a 12.0% increase from the previous year. Notably, long steel products experienced a 3.3% increase, while flat steel products saw a more substantial rise of 11.0%. Imports in December 2023 alone reached 82,230 tonnes, indicating a notable 12.3% increase compared to December 2022.

China emerged as the dominant importer, capturing 55% of total imports, particularly in HR coil/sheet & plate coil and HD galvanized sheet categories. Germany and Japan followed suit with 12% and 6% shares, respectively.

On the export front, South Africa experienced a surge in the export of primary carbon, alloy, and other steel products in 2023. The total volume reached 1,366,799 tonnes, marking a substantial 24.5% increase compared to the previous year. Notable contributors included billets, blooms, and slabs, which exhibited steady growth.