2025 Confirms Structural Weakness in South Africa’s Crude Steel Production

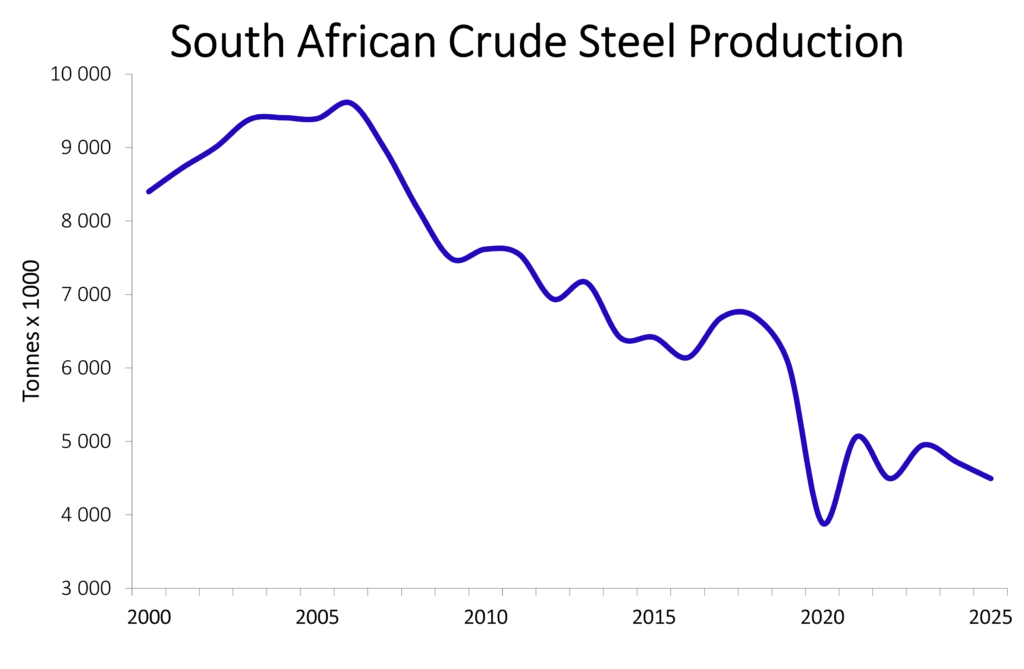

South Africa’s crude steel production in 2025 reached 4.5 million tonnes (5% down 2024), confirming that the industry remains under severe and sustained pressure, with output stabilising at levels well below historical norms.

Despite a modest recovery following the COVID-19 shock, 2025 production remains approximately 25% lower than pre-pandemic levels in 2019 and nearly 50% below the industry’s peak of 9.4 million tonnes recorded in 2004. This performance reinforces the reality that the sector has not returned to a growth trajectory and is instead operating in a state of structural contraction.

The continued weakness in 2025 reflects entrenched challenges facing the industry, including costly electricity supply, logistics inefficiencies, rising input costs, subdued domestic demand, and persistent pressure from low-priced and sub-input cost imports. These factors have constrained capacity utilisation and limit the industry’s ability to respond to demand recovery.

While crude steel production has remained broadly flat since 2022, the absence of meaningful growth in 2025 highlights the limits of recovery under current conditions. Without targeted and coordinated policy interventions, production is likely to remain suppressed, placing further strain on employment, investment, and the sustainability of domestic steelmaking capacity.

Steel is a strategic input for infrastructure development, energy transmission, manufacturing, and industrialisation. The continued underperformance of crude steel production in 2025 therefore signals broader risks to South Africa’s economic recovery and long-term development objectives.